After almost twenty years in the financial services industry, I can tell you firsthand as an attorney that estate planning is the most overlooked, misunderstood and procrastinated piece of the financial plan for most families. I can also tell you from experience why that’s usually the case: most people think putting together an estate plan is a lot more complex, costly and time-consuming than it almost always turns out to be. In fact, with just a little focus of time and resources, a family can save itself thousands of dollars and countless hours of time wasted in picking up the pieces after the death of a loved one because a viable estate plan was never put in place.

This article is part one in a short series on the aspects of estate planning. Today, we’ll touch on the very basics and will feature two important documents – the will and the trust. In a few follow-up articles, we’ll take a deeper dive into issues regarding taxes, gifting, beneficiaries, and we’ll look at which ancillary documents, in addition to wills and trusts, round out the “basic set” of estate planning documents for most families.

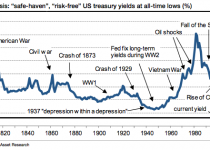

February 2015 Recap

In January, U.S. stocks posted their biggest monthly losses in a year while bond prices traded higher and market volatility surged mostly due to concerns about the lack of global growth. February experienced almost the exact opposite with U.S. stock markets hitting new highs. The S&P 500 gained 5.49%, the Dow Jones Industrial Average (DJIA) jumped 5.64%, the world’s developed stock markets gained more than 6% (EFA), and emerging markets posted solid returns as well, climbing more than 4% (EEM).