This month's models have been posted. There are CHANGES in ALL the MODELS (highlighted in yellow).

Home economics

Mortgage rates are spiking, so people are putting off buying a house. Those who already own their four walls are staying put because they know they’ll never get better loan terms than they have right now.

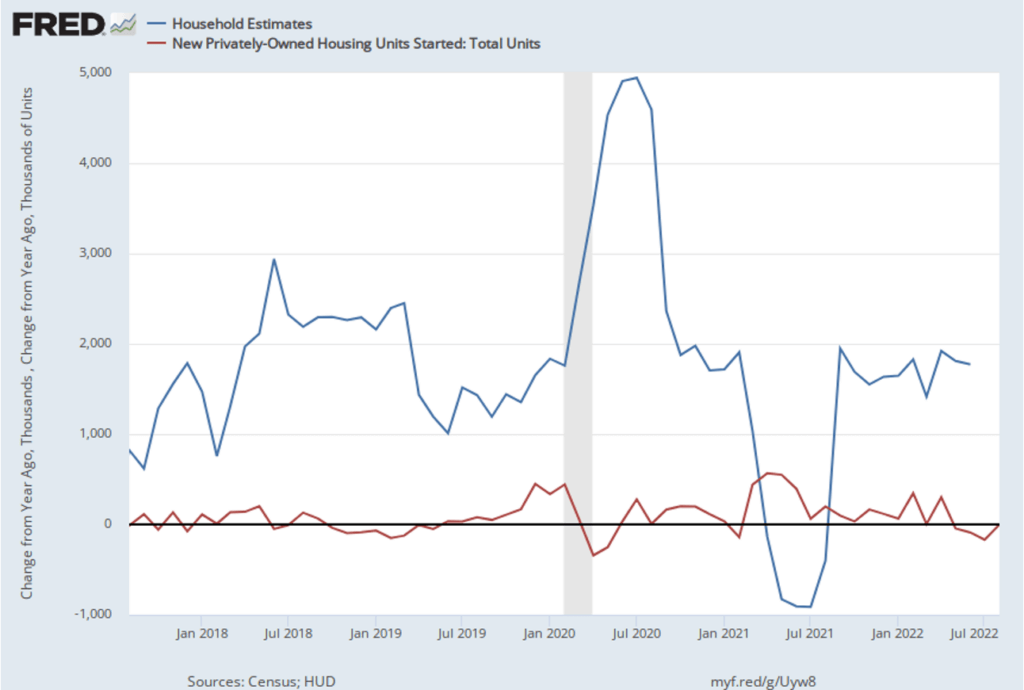

In the meantime, household formations are exceeding housing starts by about 2,000 units every 12 months. That’s actually nothing new – it’s been the persistent trend for almost five years now. The pandemic briefly accelerated that shortfall, but the demand for new homes – whether single- or multi-family – has been outstripping the supply for quite some time.

We can’t build homes fast enough. So why are prices starting to soften? Credit: Federal Reserve]

And yet, as we noted last month, home builders see their industry as already being in a recession.

The damage is contained, at least so far, in the prices of existing homes. But even there, the bad news sounds a little overblown. True, the median sales price of an existing home dropped from $413,800 in June to $389,500 in August, according to the National Association of Realtors, but that’s still higher than the $354,000 figure at the start of this year. In the meantime, monthly existing home sales have declined from 6.5 million in January to 4.8 million in August.

So, it’s not beyond the realm of possibility that the price of new homes will likewise decline in the near future. Yet ownership of even a pre-loved home remains beyond the means of many. Mortgage rates are one factor, but tight supply is at least as much to blame. Thus, people are choosing to continue renting.

The news is no better for tenants.

Rental disorders

There is clearly a price to be paid for deferring a home purchase. According to nationwide realty broker Redfin, the median asking rent breached the $2,000 per month barrier in May, for the first time in history. That median asking rate had been fairly steady in the $1,600-to-$1,700 range for years. Tenants could expect a 2%-to-4% annual hike, but for more than a year, landlords have been pushing through increases as high as 17% on average.

Of course, all real estate is local and it’s not that bad for renters in a lot of places. In a lot of other places, though, it’s even worse. Rents declined slightly in Minneapolis, Kansas City and Milwaukee. (This might be influenced by baseball fans moving out of these towns in shame, but that’s just a working theory of ours.)

Rents in Cincinnati, Seattle and Nashville, though, have increased by almost one-third in the last 12 months. But that’s nothing compared to tech magnet Austin, where leases now cost almost 50% more in May 2022 than they did in May 2021.

Rent increases have slowed down since then, but at 6% year-over-year they are still running hotter than historical norms. And in case you’re wondering why the Consumer Price Index (CPI), the most widely cited inflation gauge, keeps going up despite the recently interrupted downward trend in gas prices, rent is a major culprit.

“Rents have always been important in measures of inflation, due to their outsize share in most household budgets,” according to Bloomberg. “They comprise a little over 30% of the headline consumer price index, and about 40% of the core index.”

What next?

Whether you own or rent, prices are in flux. The general trend is still upward, but there are some troubling signs of weakness in the real estate market.

Blogger Bill McBride cautions against comparing this new vulnerability to the absolute mayhem of 2007-2009, but makes a case that it bears resemblance to the 1978-1982 realty bear market, during which inflation, combined with rising mortgage rates, eroded the desirability, and thus the value, of owning a home.

Are we really back to stagflation days and, if so, what does that mean for the market for your most valuable asset? You might want to talk to a trusted financial advisor before making any decisions about selling, buying or building.

FedEx Pilots:

Hear how Smith Anglin protects your retirement savings in this short video.

Gross domestic product declined at an annual rate of 0.6% in 2022’s second quarter, according to the third estimate released by the Bureau of Economic Analysis. This leaves the second reading’s number unchanged.

Total nonfarm payroll employment The US economy added 263,000 jobs in September, compared to a downwardly revised 315,000 in August. The unemployment rate ticked down to 3.5%, while the labor force participation rate remained steady at 62.3%. The effects of Hurricane Ian on employment statistics were minimal for the reporting period but are likely to show up in October’s data coming out soon.

Initial jobless claims The seasonally-adjusted number of Americans filing new claims for unemployment benefits increased by 29,000 to 219,000 in the week that ended October 1. The four-week moving average, which removes week-to-week volatility, increased by 250 to 206,250.

The Consumer Price Index for All Urban Consumers rose 0.4% in September on a seasonally adjusted basis after rising 0.1 percent in August, according to the Labor Department. Over the last 12 months, the all-items index increased 8.2% before seasonal adjustment. Increases in shelter, food and medical care were the largest of many contributors. These increases were partly offset by a 4.9% decline in gasoline. The core index – for all items less food and energy – rose 0.6 % in September, as it did in August.

US Stocks

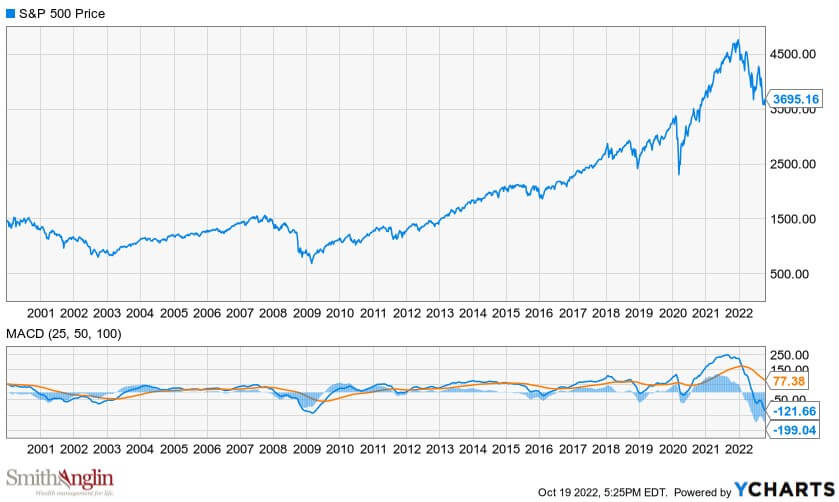

The S&P 500 dropped -9.2% in September on a total-return basis. The CBOE VIX “fear gauge” ended the month up 22.2% at 31.62. This suggests investor confidence is shaky but could be worse. The VIX was higher in the early days of the pandemic, at the peak of the 2008-09 financial crisis, and during the one-two punch of the dotcom bust and the 9/11 attacks.

International

Continental Europe followed Wall Street’s suit, with London’s FTSE 100, Frankfurt’s DAX and Amsterdam’s Euronext 100 down -5.4%, -5.6% and -6.9% respectively in September.

It was the same story in Asia. Shanghai’s SSE Composite and Tokyo’s Nikkei 225 declined -5.6% and -7.7%,respectively, while Hong Kong’s Hang Seng plummeted -13.7%.

Central Banks

The Federal Reserve has two stated mandates: Promote price stability and minimize unemployment. At the moment, the governors are focused on the first, and for good reason: We are experiencing an inflation spike and also have a hot jobs market - there are two openings available for the average job candidate. But there’s a growing consensus – both within the U.S. and globally – that the Fed is overshooting and might need to change priorities.

Let’s remember that when the Fed – the central bank associated with the U.S. dollar, the world’s most widely held reserve currency – pursues a policy, other central banks feel the pressure to make similar moves. And what’s in the immediate American interest might not be in the long-term interests of other rich countries and could actually be contrary to those of middle-income or developing economies. Both the United Nations and the World Bank have expressed their concern that the current round of interest rate hikes, intended to curb inflation here, could lead to a worldwide recession within the year.

Commodities

West Texas Intermediate crude prices continued their decline, dropping -11.2% to end September at $79.49 per barrel.

One indicator that inflation might be slowing is the price of gold. The safe harbor precious metal continued to settle lower, dipping -3.1% to end September at $1,672.00 per ounce.

The dollar gained +2.6% in Frankfurt, making it more valuable than the euro. The U.S. currency soared +4.0% in London during a month of fiscal chaos in Britain and rose +3.2% in Tokyo.

Bitcoin, the bellwether cryptocurrency, dipped a mere -3.7% to end the month at $19,501.25, making it less volatile than the stock market in September.

Is Your Card Up To Date?

Is your credit card about to expire? Have you recently received a new card? It’s easy to update your CREDIT CARD information. Just call us at 717-569-8162, or go to the Update Credit Card Information section under the Member’s Tab.

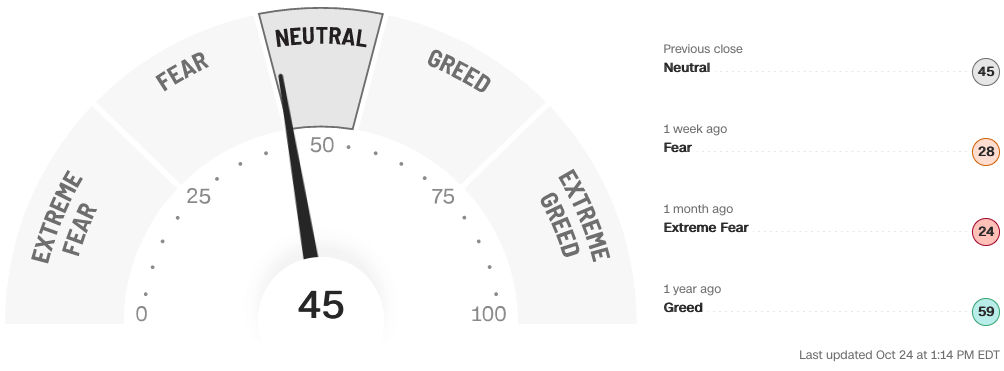

Fear & Greed Index

Bull Bear Oscillator vs. S&P 500 Index

This month’s models are now available to subscribers. If you are interested in becoming an Airline subscriber, click here or please contact us at 1-717-569-8162 or email us at airways@uspfa.org.

From the Captain's Table

The long and short on bonds

Sometimes the best stock to pick is None of the Above. This seems to be one of those times.

As you read above, the stock market lost 9.2% last month. There were few winners. US News and World Report lists the top 10 performing stocks year-to-date. You’ve probably never heard of any of them. These are not the mega-caps that attract the most attention among retail investors. They’re niche players in biotech or energy-adjacent firms that are spiking because of supply disruptions throughout the world. Maybe one or two are keepers. We’ll see.

Exxon Mobil and ConocoPhillips are the only mega-caps that have materially appreciated in the past 12 months. But let’s not lose sight of how very cyclical the Energy sector is. If history is any guide, these gains will not be locked in.

So, if stocks are so volatile to the downside, where should you be investing?

Consider bonds.

Risk and reward

Fixed-income securities are really attractive now. Again, as we noted above, the benchmark 10-year Treasury ended September at 3.8040%. Yes, that’s higher than the 3.1330% yield at the end of August but, more importantly it’s much better than the 9.2% loss average investors took on their stock portfolios in September.

Let’s factor in one more thought, though. Stocks are inherently risky. Prices go up and down constantly and sometimes dramatically. That’s what being an owner is about – tolerating risk. The expectation is that, over time, that risk will provide greater reward than fixed-income securities in your portfolio. Companies can dilute their stock with new issuance or buy it back if it’s undervalued. They can offer stock dividends and they can cancel them. But they have to pay off their debt obligations first, so there’s really very little risk in the investment-grade bond market over the long term.

And when that “company” is the U.S. federal government, that’s the ultimate “Too Big To Fail” scenario. If Uncle Sam defaults, your portfolio might be the least of your worries. So, which would you rather have: A risky investment that plummeted 9.2% last month, or a risk-free investment that paid 3.8040% per year?

One bad month – or quarter – shouldn’t cloud your judgment. Investment is about looking to the future, not the past. Stocks could snap back any time. But the smart money seems to be telling us, “not anytime soon”.

Investors today ignore the bond market at their own financial risk.

The gap

We’ve written a lot in this space about the ramifications of an inverted yield curve, when short-term notes pay higher interest rates than long-term bonds. We’re in that situation now, but let’s not overstate the case. Economist Bill Connerly wrote an interesting piece in Forbes’s online edition about how imperfect a predictor the inverted yield curve really is.

The recessions “which began in 1953 and 1957 were not preceded by yield curve inversions. So, this concept is not perfect by any means,” according to Connerly, who further notes that, in 1966 and 1986, the yield curve inverted without a recession.

It’s important to remember why the yield curve is inverted: expected inflation. Most of us believe that higher-than-accustomed price increases will be with us for the next year or so, but the future beyond that is murky. Considering the Federal Reserve’s muscular approach to taming inflation – even if it means sparking a recession – it’s doubtful that this instability will continue over the long term.

Short-term pain, long-term planning

So how should you play this?

First, you probably shouldn’t go all-in on bonds. It’s a tough position to be in if you have to live off a cash flow that is dependent on the vagaries of Fed policy. That said, buying short-term bonds is an opportunity – now – to make some extra pin money. But long term, you’ll want to match the duration of your bonds with your own time horizon.

This is complicated stuff, and it just gets more complicated. In addition to corporate and government bonds, there are also tax-advantaged municipal bonds to consider. You’d be well advised to talk with a trusted financial professional before moving into this space.

-David

David Camarillo, CFP®, ChFC, CFS

Director of Advisory Services

David is a proud Trinity University alum, where he earned his Bachelor of Arts in English and History. He started his career in the financial services industry in 2005 at Wells Fargo, and in 2007 he joined H.D. Vest Financial Services where he consulted for the company’s top financial advisors. He held a Series 7 and 66 until 2018, and he still holds life and health insurance agent and variable insurance products agent. He obtained the Certified Financial Planner™ (CFP) designation in 2011, the Chartered Financial Consultant (ChFC) designation in 2014, and holds the Certified Funds Specialist (CFS) designation. David has been a Wealth Advisor with Smith Anglin since 2014, and in 2019 he was promoted to Director of Advisory Services.

Outside the office David stays active with his wife, Mayra, and two kids, David Jr. and Amelia. David is an avid runner, racing everything from the 5k to the marathon. He enjoys hiking nature trails with his family and their dog, Bo, and playing guitar loudly when possible. He also volunteers with Back on My Feet and the North Texas Food Bank.